Fleet Tax Benefits: Leasing vs. Buying Heavy Equipment

Commercial Fleet Acquisition Strategy: A Global Analysis of Tax Depreciation, Leasing Dynamics, and Heavy Industry Asset Management

The acquisition, deployment, and lifecycle management of heavy commercial fleets represent one of the most structurally complex and capital-intensive operational requirements for entities engaged in mining, construction, logistics, and infrastructure development. For multinational heavy industry corporations, the strategic determination between purchasing capital assets outright, engaging in hire purchase agreements, or utilizing sophisticated commercial fleet leasing arrangements is a multifaceted financial calculation. It is a decision that extends far beyond the mere operational utility of the machinery, striking at the very core of corporate treasury management, balance sheet optimization, and statutory tax liability minimization. The modern fleet acquisition strategy is inexorably linked to the net present value of tax shields, the nuances of international accounting standards, and the aggressive utilization of jurisdictional tax depreciation schedules engineered by sovereign governments.

Historically, the decision to lease or buy was driven primarily by an entity’s immediate access to liquidity and the desire to mitigate the risk of asset obsolescence. However, in the contemporary macroeconomic environment, the calculus has evolved into a highly sophisticated financial modeling exercise. Heavy equipment, characterized by rapid initial depreciation, steep maintenance curves, and volatile secondary market residual values, forces financial controllers to rigorously analyze the time value of money, the weighted average cost of capital, and the specific macroeconomic tax incentives deployed to stimulate domestic industrial investment. This comprehensive analysis explores the profound financial, accounting, and tax implications of commercial fleet leasing versus purchasing, providing a definitive framework for heavy industry asset management across multiple global jurisdictions.

Foundational Financial Structures: Lease vs. Purchase Paradigms

The fundamental dichotomy in heavy fleet acquisition rests between absolute ownership and usage rights, a distinction formalized through the legal and financial frameworks of outright purchasing, capital leasing, operating leasing, and hire purchase agreements. Each mechanism carries distinct, cascading implications for cash flow generation, equity accumulation, and the timing of tax deductibility.

Finance Calculator

Use this calculator to estimate repayments or growth before you compare providers.

The Dynamics of Asset Purchasing

Purchasing heavy commercial vehicles outright or through traditional debt financing confers absolute legal and beneficial ownership to the acquiring entity. In a purchase scenario, the entity capitalizes the asset on its balance sheet, assumes the entirety of the asset’s residual value risk, and bears the comprehensive, ongoing burden of maintenance, insurance, and eventual disposal. The primary financial advantage of purchasing lies in the immediate accumulation of operational equity and the ability to aggressively leverage sovereign tax codes to shield corporate income through front-loaded depreciation deductions.

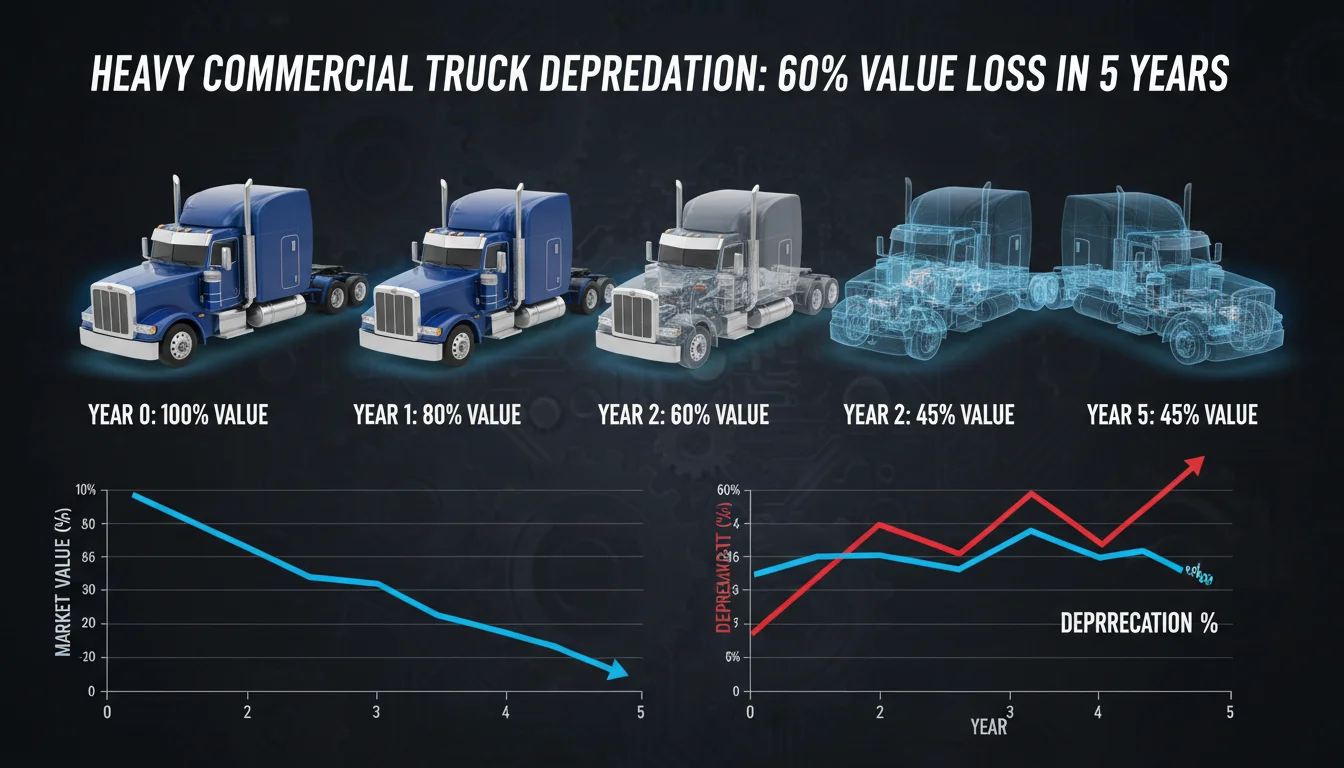

However, the massive capital expenditure required for heavy machinery purchases results in severe, immediate liquidity degradation. The high upfront costs inherently trap capital that could otherwise be deployed toward high-yield operational expansions, technological advancements, or strategic acquisitions. Furthermore, commercial trucks and heavy machinery are rapidly depreciating assets that lose value precipitously upon deployment. For instance, a new Class 8 commercial truck may forfeit between 20 percent and 30 percent of its original market value within the first twelve months of service, ultimately shedding up to 60 percent by the conclusion of its fifth year of operation. A vehicle’s depreciation rate is influenced by a complex matrix of vehicle-specific and market factors, including fuel efficiency, maintenance history, operating conditions, supply and demand elasticity, and the prevailing economic climate. Used trucks present a unique advantage in this regard, allowing operators to bypass the steepest initial depreciation drop and experience a much slower rate of value degradation than newly released models.

Capital and Finance Leases

A capital lease, synonymous with a finance lease in various global jurisdictions, is an arrangement that functions economically as a debt-financed purchase, despite the legal title frequently remaining with the lessor until the conclusion of the lease term. Under a finance lease, the lessor transfers substantially all the risks and rewards incidental to ownership of the heavy vehicle to the lessee.

Because the economic substance of the transaction fundamentally mirrors ownership, the lessee must account for the leased fleet as both an asset and a corresponding liability on the corporate balance sheet. Consequently, the lessee assumes the comprehensive responsibility for maintaining, repairing, and insuring the leased vehicles, acting as the de facto owner throughout the duration of the contract. The critical strategic advantage of the capital lease for heavy industry lies in asset accumulation without the catastrophic initial capital outlay. The lessee treats the transaction as a purchase for accounting and tax purposes, thereby unlocking the ability to claim statutory tax depreciation on the asset and deduct the interest portion of the lease payments as a business expense. This dual tax shield—comprising both interest expense deductions and accelerated depreciation—provides profound long-term tax savings, making capital leases highly advantageous for businesses with predictable, long-term fleet requirements that seek to build asset equity over time.

Furthermore, capital leases frequently incorporate a Terminal Rental Adjustment Clause (TRAC) or a guaranteed residual value mechanism. By allowing the lessee to retain the residual value of the vehicle at the end of the lease term, capital leases strongly incentivize rigorous maintenance protocols and offer a potential payout or a highly reduced acquisition fee to secure final legal ownership. Over time, the slightly higher monthly payments associated with capital leases—which account for the full price of the vehicle without initially factoring in depreciation—build up the lessee’s equity position, culminating in full asset ownership.

Hire Purchase Agreements

Distinct from traditional finance leases, the hire purchase agreement represents a highly prevalent financing modality in jurisdictions such as Nepal, India, and the United Kingdom. A hire purchase is essentially a conditional financing agreement wherein the entity utilizes an asset while paying for it in structured installments. It operates akin to a rent-to-own mechanism characterized by specific legal parameters.

In a hire purchase agreement, the acquiring entity does not actually obtain legal ownership of the heavy machinery until the final installment is completed and a specific “option to purchase” fee is paid, which formally transfers the legal title. Until that terminal payment is executed, the entity is technically “hiring” the asset, while the seller or finance company retains legal ownership. However, much like a finance lease, the hirer is entirely responsible for the care, maintenance, and insurance of the item.

Crucially, if the hirer fails to fulfill the installment obligations, the seller retains the explicit legal right to repossess the heavy equipment. From a taxation standpoint, the distinction is paramount. Despite lacking ultimate legal title during the payment period, tax authorities generally recognize the hirer as the beneficial owner for tax purposes. This allows the hirer to claim the statutory depreciation allowances on the asset, while the financing charges inherent in the hire installments are taxed as the hire-vendor’s income and allowed as the hirer’s deductible interest expense.

The Operating Lease Framework

Conversely, the operating lease is historically structured as a pure rental or usage agreement. The lessor retains absolute legal ownership, assumes the risk of residual value fluctuation, and claims the statutory tax depreciation. The lessee is granted the right to utilize the heavy machinery for a fraction of its useful economic life, paying a regular, fixed lease expense.

For rapidly growing fleets or entities navigating volatile macroeconomic environments, the operating lease offers unparalleled flexibility and cost efficiency.

Operating leases inherently feature lower monthly cash outflows compared to capital leases, hire purchases, or debt-financed acquisitions because the lessee is effectively financing only the anticipated depreciation of the asset during the lease term, rather than its entire capital cost. This structure radically reduces upfront capital requirements, preserving corporate liquidity and stabilizing cash flows for investments in technology or operational improvements.

Furthermore, operating leases frequently relieve the lessee of the administrative burdens associated with complex fleet maintenance, while spreading out rental taxes over time as part of the monthly payments rather than requiring a massive one-time payment on the vehicle’s total cost. The entire lease payment is typically fully tax-deductible as an operating expense in the period it is incurred, providing a stable, predictable tax shield across the lifecycle of multiple vehicles, which is often the superior strategy for entities seeking stable deductions rather than massive, one-time write-offs.

The Global Accounting Transformation: IFRS 16 and ASC 842

For decades, the historical preference for operating leases in heavy industry was heavily predicated on the ability to keep massive fleet liabilities entirely hidden in the footnotes of financial statements rather than prominently displayed on the balance sheet. This opacity, permitted under legacy standards like IAS 17 and FASB Topic 840, severely hindered the ability of investors, analysts, and credit rating agencies to accurately assess the leverage and true financial commitments of capital-intensive industries such as transportation, logistics, and construction. To rectify this systemic lack of transparency, global accounting standard-setters introduced sweeping, paradigm-shifting reforms: International Financial Reporting Standard 16 (IFRS 16) and Accounting Standards Codification Topic 842 (ASC 842).

The Mechanics of Balance Sheet Capitalization

The implementation of IFRS 16 (effective January 1, 2019) and ASC 842 mandated that lessees recognize nearly all leases, including operating leases, on the balance sheet. Heavy industry entities are now strictly required to capitalize a “Right-of-Use” (ROU) asset, which reflects their contractual right to utilize the leased machinery for a period of time, alongside a corresponding lease liability representing the present value of future lease payments.

This transition fundamentally altered the balance sheets of asset-heavy corporations globally. Extensive surveys of corporate impacts revealed that sectors reliant on transport, shipping, and airlines witnessed their total reported assets artificially inflate by an average of 14 percent simply due to the capitalization of previously off-balance-sheet operating leases, while telecommunications saw a 6 percent increase. Consequently, gearing ratios and leverage metrics increased dramatically, while return on capital employed (ROCE), return on equity (ROE), and asset turnover ratios artificially deteriorated due to the massively inflated denominator. This accounting paradigm shift has forced treasury departments to meticulously renegotiate debt loan covenants and borrowing costs to prevent technical defaults triggered purely by statutory accounting changes.

Divergence Between IFRS 16 and ASC 842

While both IFRS 16 and ASC 842 aim to increase transparency by bringing leases onto the balance sheet, they diverge significantly in their structural treatment of the lessee income statement and cash flow classifications, creating complex reconciliation requirements for multinational heavy industries and dual reporters.

IFRS 16 applies a single, unified lessee accounting model. Under this regime, the classification of an operating lease is entirely eliminated for the lessee; nearly all leases are accounted for in the exact same manner as traditional finance leases. The lessee recognizes the depreciation amortization of the ROU asset and the interest expense on the outstanding lease liability. This has a profound impact on corporate profitability metrics. Because the traditional single “rent expense” is removed from operating expenses and replaced by depreciation and interest (both of which fall below the operating profit line), entities reporting under IFRS 16 experience a massive, artificial inflation of Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA). Furthermore, cash flow classification changes, with principal payments moving to financing activities and interest to operating or financing, enhancing reported operating cash flows.

Conversely, US GAAP’s ASC 842 retains a dual-model approach, distinguishing between finance leases and operating leases for income statement treatment. While operating leases are brought onto the balance sheet as ROU assets, the lease expense is still recognized on a straight-line basis over the lease term within standard operating expenses. Consequently, operating leases under ASC 842 directly reduce EBITDA, whereas the exact same lease under IFRS 16 would inflate reported EBITDA. For investors and lenders comparing cross-border heavy equipment operators, this presentation difference requires meticulous adjustment to ensure parity in covenant testing and performance evaluation, even when the underlying economic realities of the fleets are identical.

Further critical divergences exist in scope, measurement, and practical expedients:

- Low-Value Exemptions: IFRS 16 explicitly permits an exemption for low-value assets, allowing them to remain off the balance sheet. ASC 842 provides no such low-value exemption, which creates a highly meaningful administrative and balance sheet scope impact for heavy industries that lease thousands of small tools or auxiliary equipment alongside their heavy fleets.

- Intangible Assets: Scope differences can be mitigated by electing not to apply IFRS 16 to certain leases of intangible assets, primarily because leases of intangible assets are entirely excluded from the scope of ASC 842.

- CPI-Linked Payments: Under IFRS 16, if lease payments are tied to an index or rate (e.g., adjusted annually for the Consumer Price Index), the lease liability is strictly remeasured each year to reflect the current CPI. Under ASC 842, the liability is not remeasured for changes in the CPI unless remeasurement is required for a fundamental reason like a change in the lease term; instead, the variable increases are simply expensed as incurred.

- Sales Taxes and Lessor Costs: ASC 842 offers lessors a practical expedient permitting them to present sales taxes collected from lessees on a net basis, and mandates that lessor costs paid directly to a third party by a lessee be excluded from variable payments.

| Accounting Feature | IFRS 16 (International Standards) | ASC 842 (US GAAP) |

|---|---|---|

| Lessee Accounting Model | Single Model (All treated as finance leases) | Dual Model (Operating vs. Finance distinction retained) |

| Balance Sheet Impact | ROU Asset & Lease Liability Recognized | ROU Asset & Lease Liability Recognized |

| Income Statement Treatment | Depreciation of ROU Asset + Interest on Liability | Single Straight-Line Lease Expense |

| EBITDA Impact | Increases reported EBITDA (Expenses fall below line) | Reduces EBITDA (Expense stays above line) |

| Variable CPI Payments | Liability remeasured annually reflecting current CPI | Expensed as incurred; no liability remeasurement |

| Low-Value Asset Exemption | Permitted (Keeps small tools off balance sheet) | Not Permitted (Meaningful practical impact) |

| Intangible Assets Scope | Generally included (but election to exclude possible) | Excluded from scope |