Singapore Wealth Management & Asset Protection 2026

Singapore Private Wealth Management: Asset Protection and Succession Planning for High-Net-Worth Families in 2026

The Evolution of the Asian Wealth Management Paradigm

The private wealth management landscape in the Asia-Pacific region is currently undergoing a profound structural transformation. Driven by an unprecedented intergenerational wealth transfer estimated at USD 5.8 trillion between 2023 and 2030, ultra-high-net-worth (UHNW) families are rapidly pivoting from rudimentary offshore wealth accumulation to highly institutionalized models of wealth stewardship. Within this macroeconomic context, Singapore has firmly established itself as the preeminent wealth management hub in Asia, frequently competing with—and increasingly outpacing—traditional jurisdictions such as Switzerland, Hong Kong, and Dubai. The concentration of private capital in the city-state is evidenced by the proliferation of Single Family Offices (SFOs), which surged from approximately 400 in 2020 to well over 2,000 by the end of 2024, continuing a steep upward trajectory into 2026.

This ascent is not an accidental byproduct of global capital flight, but rather the result of Singapore’s deliberate synthesis of political stability, robust English common law jurisprudence, and a highly calibrated regulatory and tax architecture. Historically, multinational groups and UHNW families utilized offshore centers primarily for tax arbitrage. However, the global macroeconomic environment of 2026 presents novel challenges. The implementation of the Organisation for Economic Co-operation and Development (OECD) Base Erosion and Profit Shifting (BEPS) 2.0 Pillar Two framework, which enforces a 15% global minimum tax on large multinational enterprises, has fundamentally altered cross-border capital allocation. As tax opacity diminishes globally, the value proposition of the Singapore wealth management hub has transcended pure tax minimization. UHNW families are increasingly utilizing the jurisdiction for its legal certainty, advanced corporate structures like the Variable Capital Company, robust trust firewalls against forced heirship, and comprehensive family governance frameworks.

To maintain its competitive edge and support the domestic economy amidst global volatility, the Singapore government introduced targeted fiscal measures in Budget 2026. These include a 40% Corporate Income Tax (CIT) rebate (capped at SGD 30,000) for active companies, extensive investments in artificial intelligence (AI) infrastructure with a 400% tax deduction for AI spending, and deep liquidity injections into the domestic equities market. Furthermore, regulatory bodies have shifted their focus from merely attracting capital to ensuring that incoming wealth creates substantive economic spillover.

Finance Calculator

Use this calculator to estimate repayments or growth before you compare providers.

The resulting paradigm requires family principals, chief investment officers, and wealth advisors to navigate a complex matrix of regulatory compliance, asset protection, and succession planning. Capital must now be structured not just for growth, but for intergenerational resilience, regulatory transparency, and alignment with modern environmental and technological standards. The following analysis deconstructs the essential mechanisms, legislative frameworks, and strategic corollaries of operating a private wealth enterprise in Singapore as of 2026.

Fiscal Architecture and Regulatory Revisions for Family Offices

The foundation of Singapore’s appeal to international wealth lies in its targeted fund tax incentive schemes under the Income Tax Act 1947. Specifically, Sections 13O (Singapore Resident Fund Scheme) and 13U (Enhanced Tier Fund Scheme) provide complete tax exemptions on “specified income” derived from “designated investments”. In practice, this covers a broad scope of income derived from a wide range of global investments, effectively shielding family portfolios from domestic capital gains and income taxes. Recognizing the importance of these structures, the government has extended the 13O, 13U, and 13D schemes, along with associated Goods and Services Tax (GST) remissions and withholding tax exemptions, through December 31, 2029, providing long-term structural certainty.

However, to ensure that this influx of foreign capital yields tangible economic benefits for the domestic market, the Monetary Authority of Singapore (MAS) has progressively tightened the qualifying criteria. The modernization of the tax incentive criteria reflects a strategic shift by the MAS to serve as a “quality filter,” prioritizing deep economic anchoring over mere volume aggregation.

Enhanced Economic Criteria for Section 13O and 13U

The revised frameworks demand significantly greater economic substance from family offices, specifically targeting domestic expenditure, professional employment, and local capital deployment. Furthermore, the introduction of Section 13OA accommodates Limited Partnership (LP) structures, applying similar criteria to Section 13O but allowing tax exemption at the partnership level, thereby expanding the structuring options beyond standard corporate entities.

- Minimum AUM: For Section 13O / 13OA, SGD 20 million is required at application and must be maintained at the end of each Financial Year (FY). For Section 13U, the requirement is SGD 50 million at application and maintained at the end of each FY.

- Investment Professionals (IPs): Section 13O / 13OA requires a minimum of 2 IPs, where at least 1 must be a non-family member. They must be Singapore tax residents earning at least SGD 3,500/month. Section 13U requires a minimum of 3 IPs, with at least 1 being a non-family member, and all must hold relevant qualifications.

- Local Business Spending (LBS): Section 13O / 13OA requires a minimum of SGD 200,000 annually, while Section 13U requires a minimum of SGD 500,000 annually, both subject to a tiered framework based on total AUM.

- Capital Deployment Requirement (CDR): For both schemes, 10% of AUM or SGD 10 million (whichever is lower) must be deployed in local designated investments.

- Corporate Structure: Section 13O is restricted to Singapore-incorporated companies or Limited Partnerships (13OA). Section 13U is structure-agnostic and can utilize offshore entities, master-feeder, or SPV structures.

A critical development effective January 1, 2025, is the strict enforcement of the Assets Under Management (AUM) maintenance. Previously, the minimum fund size requirement only applied at the point of application. Under the updated regime, funds must demonstrate compliance at the close of every financial year. For open-ended funds facing volatile markets or sudden family redemptions, this creates a persistent risk of breaching the threshold and losing tax-exempt status for that Year of Assessment (YA).

To mitigate this operational friction, MAS introduced a relief mechanism for funds with fixed lifespans. Closed-end funds can make an irrevocable election for “closed-end fund treatment”. This election waives the annual AUM requirement entirely from the sixth incentive year onward and allows the Local Business Spending requirement to be calculated cumulatively up to the tenth incentive year. This structural nuance is indispensable for family offices executing J-curve investment strategies, allowing them to return capital to the family without triggering a loss of tax incentives.

The Capital Deployment Requirement (CDR) and Master-Feeder Consolidation

The Capital Deployment Requirement (CDR) mandates that a portion of the family’s wealth directly interfaces with the Singaporean economy. Funds must deploy the lower of SGD 10 million or 10% of their AUM into domestic assets, including equities listed on MAS-approved exchanges, qualifying debt securities, non-listed funds distributed by local licensed financial institutions, or direct investments into unlisted Singapore operating companies. Reflecting Singapore’s broader macroeconomic priorities, the eligible investment list has been expanded to include climate-related investments and blended finance structures. Notably, investments in environmental attribute certificates and specific green bonds are granted multipliers toward fulfilling the CDR quota.

For larger, highly sophisticated family offices utilizing the Section 13U scheme, the regulatory burden of maintaining these thresholds across multiple entities has been streamlined. Master-feeder funds and master-SPV structures can now submit a consolidated tax incentive application. Consequently, the AUM and LBS requirements apply at the level of the aggregate structure as a single fund entity, eliminating the requirement to multiply these figures for every Special Purpose Vehicle (SPV) added to the corporate tree.

The Global Investor Programme (GIP) Alignment

For UHNW individuals seeking Singapore Permanent Residency (PR) in tandem with wealth structuring, the Global Investor Programme (GIP) administered by the Economic Development Board (EDB) has been drastically restructured.

The GIP accords PR status to eligible global investors who drive business and investment growth. Under the revised 2026 framework, the barriers to entry have been raised exponentially.

Option C (the Family Office route) now mandates that applicants establish a Singapore-based SFO with at least SGD 200 million in total AUM, representing the family’s total investable wealth. More critically, applicants must deploy a minimum of SGD 50 million into local “Designated Investments” within 12 months of PR approval. As of the 2025/2026 equity policy updates, this SGD 50 million deployment is now heavily restricted: it must be allocated directly into equities listed on approved Singapore exchanges (SGX).

This non-negotiable S$50 million equity sleeve directly serves the government’s macroeconomic objective of deepening liquidity and broadening participation in local capital markets. Real Estate Investment Trusts (REITs) and Business Trusts no longer qualify toward this mandatory allocation, forcing family office Chief Investment Officers (CIOs) to formalize active SGX-equity investment sleeves, establish manager-selection criteria, and coordinate complex liquidity guardrails within their portfolio construction.

The Institutionalization of the Family Office Ecosystem

The rapid expansion of the family office sector has necessitated a commensurate evolution in regulatory oversight. Operating a private wealth vehicle in Singapore requires navigating intricate licensing exemptions and anti-money laundering (AML) frameworks. As the market matures, the regulatory posture has shifted from permissive attraction to rigorous institutionalization.

The MAS Class Exemption Framework

Historically, SFOs operated in a regulatory grey area. They relied on a legal interpretation of the Securities and Futures Act (SFA), claiming an exemption from the Capital Markets Services (CMS) license by arguing they were providing fund management services strictly to a “related corporation”. To formalize this and address potential money laundering risks, MAS introduced a dedicated class exemption framework specifically for SFOs.

Under the finalized guidelines, to operate without a CMS license, an SFO must meet strict qualifying criteria: it must be wholly owned and controlled by members of the same family, be incorporated in Singapore, establish and maintain a business relationship with a MAS-regulated bank, and appoint at least one Singapore-resident employee to act as a primary liaison with the regulator.

The definition of “family” has been carefully structured to prevent abuse while accommodating legitimate intergenerational planning. It is bound by a definitive generational limit: the common ancestor must not be more than five generations back from the youngest generation that established the SFO in Singapore. All family members within these five generations can be served, and the definition expansively includes parents-in-law, siblings-in-law, legally adopted children, and stepchildren.

Crucially, the MAS explicitly prohibited exempt SFOs from managing third-party monies. This prohibition extends to charitable organizations that receive donations from third parties, as allowing SFOs to manage such funds would be inconsistent with the rationale for a private class exemption that lacks the safeguards required for third-party retail customers. Furthermore, SFOs are prohibited from functioning as internal treasury or cash management platforms for their operational corporate groups, strictly preserving the vehicle for private family investment wealth.

Optimized Screening and the Corporate Service Providers Act

A significant operational bottleneck for SFO setup in 2023 and 2024 was the extensive background check process. Previously, new family office applications were required to submit third-party background check reports issued by designated private service providers, a process that frequently extended approval timelines to upwards of 18 months.

To resolve this inefficiency and enhance data security, MAS enacted a major policy shift effective January 1, 2026. The requirement for third-party reports was eliminated; instead, background assessments and source-of-wealth verifications are now conducted directly by internal MAS teams. By bringing these assessments in-house, MAS drastically reduced the risk of sensitive family asset information leaking through external vendors, while simultaneously shortening overall approval timelines and lowering the financial burden on applicants.

Concurrently, the broader corporate governance landscape was transformed by the Corporate Service Providers (CSP) Act, which came into full effect in June 2025. All businesses providing corporate services—including company formation, registered addresses, and the provision of nominee directors—must now register with the Accounting and Corporate Regulatory Authority (ACRA).

Crucially for family offices that rely on nominee arrangements to maintain operational privacy, the CSP Act mandates rigorous fit-and-proper testing for all nominee directors and prohibits individuals from acting as nominee directors by way of business unless arranged through a registered CSP. Furthermore, companies are now required to maintain registers of nominee directors and shareholders and submit this information to ACRA, where the nominee status is made publicly available.

This legislative maneuver aligns Singapore with the Financial Action Task Force (FATF) standards on beneficial ownership. The structural implication for UHNW families is the creation of a dual-layered privacy system: while the ultimate beneficial owners (UBOs) may remain shielded behind complex corporate trust layers, the regulatory transparency demanded from the service providers and the public flagging of nominee status ensures that illicit actors cannot utilize shell companies to obfuscate capital. Breaches of AML/CFT obligations by CSPs now carry severe criminal fines of up to SGD 100,000, ensuring that the foundational infrastructure supporting SFOs maintains the highest global compliance standards.

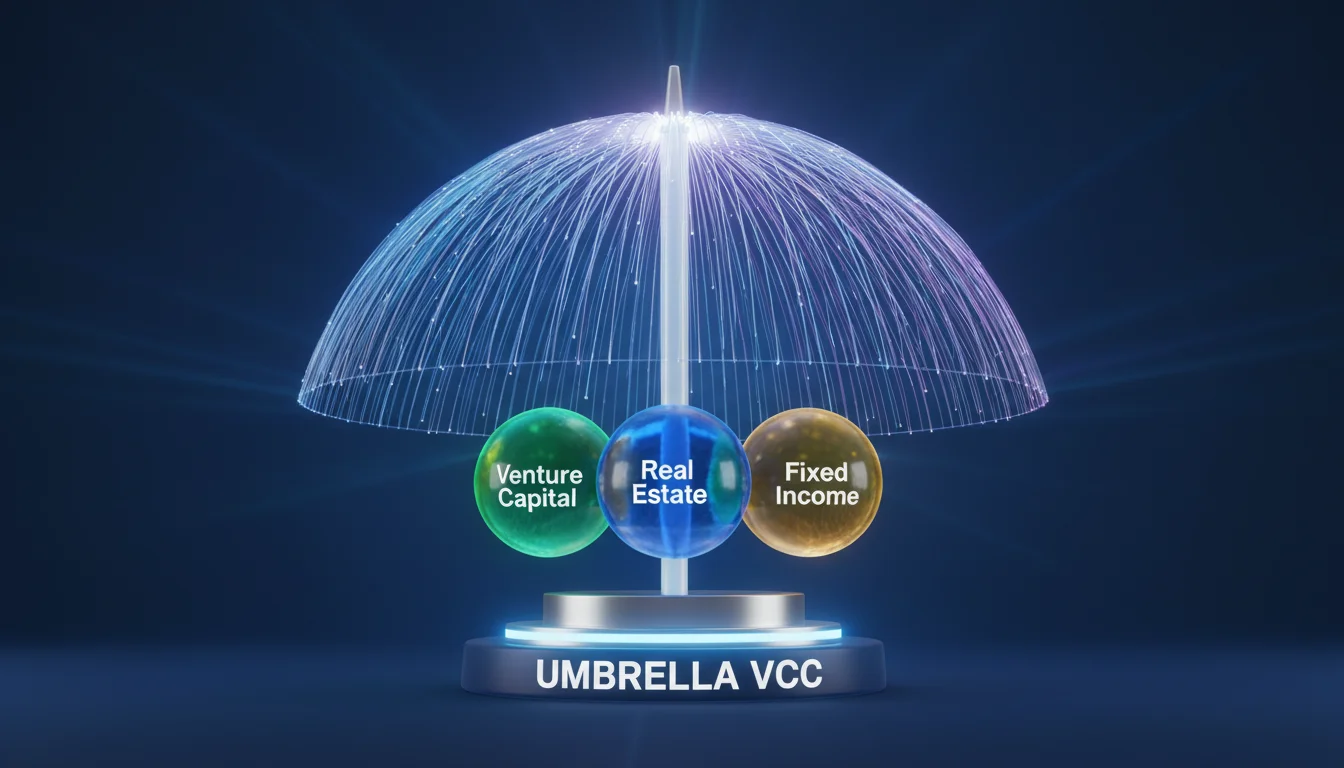

Structural Innovation: The Variable Capital Company Framework

While SFOs provide the advisory and management overlay, the actual pooling and deployment of capital requires a robust legal container. Introduced in 2020 and continually refined through 2026, the Variable Capital Company (VCC) is a specialized corporate structure that has rapidly become the vehicle of choice for sophisticated asset management and family offices. Designed to rival the premier fund structures of the Cayman Islands, Dublin, and Luxembourg, the VCC fundamentally alters how private wealth can be segregated, administered, and scaled.

Structural Mechanics and Statutory Asset Segregation

A VCC is a distinct legal entity tailored explicitly for investment funds, meaning it cannot be used for standard operating businesses. It can be established as a standalone fund or as an umbrella structure containing multiple sub-funds. For UHNW families managing complex, multi-generational wealth, the umbrella VCC offers profound architectural advantages. A single legal entity can house disparate sub-funds, each with its own distinct investment strategy, asset class, or designated family branch.

The defining feature of the umbrella VCC is statutory ring-fencing. The assets and liabilities of one sub-fund are legally segregated from those of another. Consequently, if a sub-fund dedicated to high-risk venture capital or leveraged real estate investments incurs severe liabilities or faces insolvency, creditors are legally barred from attaching the assets of a separate sub-fund holding the family’s conservative fixed-income portfolio or core heirloom assets.

Furthermore, the umbrella structure provides significant operational economies of scale. Sub-funds share a common board of directors, fund manager, corporate secretary, and auditor, radically reducing the administrative burden, duplication of costs, and time-to-market compared to maintaining a web of distinct holding companies across multiple jurisdictions.

Capital Agility, Privacy, and Tax Efficiency

Traditional corporate entities governed by the Singapore Companies Act face rigid, time-consuming restrictions regarding capital reduction, and dividend distributions must typically be paid out of accumulated profits. The VCC overrides these limitations. By definition, its capital is variable; shares can be seamlessly issued or redeemed based on the fund’s Net Asset Value (NAV), and crucially, dividends can be paid directly from capital. This operational agility allows family offices to execute rapid liquidity events, accommodate investor movements within the family, or rebalance portfolios without triggering complex corporate restructuring processes or shareholder approvals.

Privacy remains a paramount concern for global families navigating a transparent world.

Unlike standard Singapore private limited companies, a VCC is completely exempt from the requirement to publicly disclose its shareholder register to ACRA. Financial statements of the VCC are also not publicly retrievable. This shields the identities of the family members, their respective capital allocations, and the specific performance of their sub-funds from public scrutiny, hostile litigants, or commercial competitors.

From a tax perspective, VCCs are treated as a single corporate entity for income tax purposes, meaning an umbrella VCC only needs to submit a single tax return to the Inland Revenue Authority of Singapore (IRAS). They can readily apply for the Section 13O and 13U tax exemptions, and can also access Singapore’s extensive network of over 80 Double Taxation Agreements (DTAs) by applying for a single Certificate of Residence (COR) in the name of the umbrella entity.

The Evolution Toward VCC 2.0

Currently, a critical regulatory constraint exists: a VCC must be managed by a “Permissible Fund Manager”—an entity holding a CMS license or formally registered with MAS as a regulated financial institution. This precludes an exempt SFO from directly managing a VCC, as SFOs are specifically exempted from holding a CMS license. In practice, families must currently establish a Multi-Family Office (MFO) structure, utilize a bank-backed VCC platform (such as those offered by DBS or Schroders), or engage a licensed external asset manager to fulfill the regulatory mandate.

However, recognizing this friction, MAS has engaged in extensive industry consultations regarding a “VCC 2.0” framework. One of the primary features being explored is the expansion of the definition of permissible fund managers to explicitly include license-exempt SFOs. If fully enacted, this amendment will allow a single family to internalize the management of a VCC structure under their existing 13O or 13U tax incentive schemes, seamlessly merging the tax efficiency and bespoke control of the SFO with the unparalleled structural superiority of the VCC.

| Feature | Traditional Private Limited Company | Variable Capital Company (Umbrella) |

|---|---|---|

| Asset Segregation | Assets and liabilities are pooled across the entity. | Statutory ring-fencing between individual sub-funds. |

| Dividend Distribution | Permitted only out of retained profits. | Permitted out of capital and profits. |

| Privacy | Shareholder register is publicly accessible via ACRA. | Shareholder register and financials are kept entirely private. |

| Capital Alteration | Requires complex administrative procedures and approvals for capital reduction. | Shares are issued and redeemed fluidly based on current NAV. |

| Management Requirement | Managed by standard Board of Directors. | Must currently be managed by a Permissible Fund Manager (CMS licensed). |

Trust Jurisprudence: The Ultimate Fortress for Asset Protection

While corporate structures like the VCC govern the operational deployment of capital, the Singapore trust framework serves as the ultimate legal fortress for long-term asset protection and succession planning. Rooted in English common law but heavily modernized through statutory amendments, the jurisdiction’s trust architecture has been customized to address the distinct vulnerabilities of international UHNW families. A properly constituted trust divorces the legal ownership of an asset (held by the trustee) from the beneficial ownership (enjoyed by the family), thereby shielding the wealth from probate delays, estate fragmentation, and external creditor claims.

Firewall Provisions and Anti-Forced Heirship

A primary existential risk for global families—particularly those domiciled in civil law jurisdictions (e.g., continental Europe, Latin America, Japan) or those subject to Islamic Faraid law (e.g., Indonesia, Middle East)—is the imposition of forced heirship. Forced heirship regimes mandate that a predetermined percentage of an estate must pass to specific relatives upon death, effectively stripping the wealth owner of their testamentary freedom and threatening the continuity of closely held family businesses.

Singapore neutralizes this risk through explicit statutory “firewalls.” Under Section 90 of the Trustees Act, if a settlor possesses the legal capacity to create a trust or transfer property during their lifetime, no foreign rule relating to inheritance or succession can affect the validity of the trust or the asset transfer. The statute expressly prioritizes Singapore law over the laws of the settlor’s domicile or nationality, provided the trust is expressed to be governed by Singapore law and the trustees are resident in Singapore.

The Singapore Court of Appeal validated the robustness of this firewall in landmark jurisprudence such as Shafeeg bin Salim Talib v Fatimah bte Abud bin Talib. The Court confirmed that lifetime settlements into a trust remove the assets from the deceased’s estate, entirely bypassing local or foreign Islamic inheritance dictates. This allows a patriarch from a forced-heirship jurisdiction to consolidate multinational assets within a Singapore trust, ensuring the family enterprise passes intact according to the trust deed rather than being forcibly fragmented among heirs under local succession laws.

The Calculus of Reserved Powers and the “Sham Trust” Risk

A fundamental tension in trust law exists between the settlor’s desire to maintain control over their life’s work and the strict legal requirement to alienate assets to achieve protection. Traditionally, handing absolute discretionary control of a family business to an independent institutional trustee generated profound discomfort for entrepreneurial wealth creators. Institutional trustees are also generally reluctant to accept active, operating businesses as trust assets due to the associated management liabilities and reputational risks.

Addressing this impasse, Section 90 of the Trustees Act expressly permits a settlor to reserve “any or all powers of investment or asset management functions” without rendering the trust or settlement invalid. This statutory carve-out allows the patriarch or matriarch to continue directing the trust’s underlying business operations, vetoing specific investments, or managing the family’s SFO portfolio, while the professional trustee retains legal title to the assets and handles administration.

However, the reliance on reserved powers carries profound risks if over-utilized. The judicial doctrine of the “sham trust” or “illusory trust” remains a potent threat to asset protection. If the powers retained by the settlor are so absolute that they are “tantamount to ownership,” the trust will fail. In such scenarios, the protective veil is pierced, and creditors or hostile litigants can attach the assets.

Recent Singapore jurisprudence underscores this peril. In the 2025 High Court decision Jenny Prawesti v Sauw Tjiauw Koe, the court highlighted the catastrophic consequences of utilizing ambiguous family holding arrangements or “borrowing names” without establishing clear, contemporaneous trust documentation, resulting in protracted and emotionally devastating litigation over a multi-million dollar property portfolio. Similarly, in cases like Gaye Williams Nee Marks v Cary Donald Williams, the court disregarded a trust where the settlor retained excessive powers to remove and appoint trustees and beneficiaries simultaneously. Consequently, best practices dictate that reserved powers should be strictly limited to investment management, leaving dispositive powers (the ability to distribute capital or alter the beneficiary class) firmly in the hands of the independent fiduciary.

Private Trust Companies (PTCs) as a Governance Solution

To mitigate the risks of excessive reserved powers while maintaining familial oversight and privacy, UHNW families frequently establish Private Trust Companies (PTCs). A PTC is a bespoke corporate entity incorporated solely to act as the trustee for a specific family’s connected trusts.

By structuring the PTC’s board of directors to include a mix of senior family members and trusted professional advisors, the family retains profound, institutionalized influence over governance and administrative decisions without the settlor holding direct statutory reserved powers in their personal capacity. This neutralizes the “sham trust” argument while allowing for rapid commercial decision-making regarding family assets.

PTCs in Singapore are exempt from the onerous requirement of holding a trust business license under the Trust Companies Act, provided they act exclusively for related trusts and appoint a licensed trust company to administer mandated AML and compliance obligations. To avoid tax and probate complications associated with individual family members owning the shares of the PTC, the shares are commonly held by a separate Purpose Trust, ensuring seamless continuity of the trustee entity across generations.

The Commissioner of Trust Enforcement (CTE)

While trusts provide defense against civil creditors and familial disputes, they are not a shield against state regulatory scrutiny. Effective June 20, 2025, the Mutual Assistance in Criminal Matters (Amendment) Act 2024 fundamentally modernized trust oversight with the establishment of the Office of the Commissioner of Trust Enforcement (CTE) under the Ministry of Law.

Equipped with expansive statutory powers of investigation, examination, search, and seizure, the CTE acts as the regulatory vanguard against the misuse of trusts for illicit finance, money laundering, or terrorism financing. Under the updated Trustees (Transparency and Effective Control) Regulations, trustees face highly stringent record-keeping obligations.

They must take proactive steps to obtain and independently verify information regarding the effective controllers of the trust, including settlors, protectors, and beneficiaries. Furthermore, trustees are now legally mandated to disclose their status when entering into business relationships or prescribed transactions—a requirement that has been explicitly expanded to include interactions with real estate developers. Breaches of these obligations, or the provision of false information to the CTE, are now punishable by escalated criminal fines of up to SGD 25,000. This regulatory tightening ensures that while Singapore trusts protect assets from civil fragmentation, the jurisdiction complies flawlessly with international FATF transparency standards, preserving the integrity of the financial center.

Strategic Integration of Insurance Wrappers: PPLI and VUL

As the global tax landscape becomes increasingly aggressive, relying solely on offshore companies and trusts may generate adverse tax consequences for beneficiaries who reside in high-tax jurisdictions (such as the United States, the United Kingdom, or the European Union). To neutralize these cross-border tax liabilities while maximizing compound growth, sophisticated family offices heavily integrate Private Placement Life Insurance (PPLI) and Variable Universal Life (VUL) policies into their holding structures.

The Mechanics and Tax Efficiency of PPLI

PPLI is not a traditional retail insurance product; it is a bespoke, institutionally priced wealth-structuring wrapper designed explicitly for UHNW individuals and accredited investors. Unlike retail variable life insurance, which limits policyholders to a narrow menu of mutual funds, PPLI is entirely open-architecture. The policyholder pays a substantial premium—which can be funded via cash, bankable securities, or even non-bankable assets like real estate or private equity—and the insurance carrier opens a dedicated, segregated policy account.

Crucially, the underlying assets within the PPLI wrapper are managed on a discretionary basis by an appointed asset manager, which is frequently the family’s own SFO utilizing the Section 13O or 13U tax incentive frameworks.

The strategic brilliance of PPLI lies in its legal classification. Because the underlying assets are legally owned by the insurance company rather than the individual or the family trust, all capital gains, dividends, and interest generated within the policy compound in a tax-deferred (and often entirely tax-free) environment. In high-tax jurisdictions, this eliminates the drag of annual capital gains taxes, significantly accelerating the compounding of wealth over a multi-decade horizon.

| Characteristic | Traditional Corporate / Trust Holding | PPLI / VUL Wrapper |

|---|---|---|

| Tax Treatment of Gains | Subject to local corporate taxation; potentially taxable upon distribution to resident beneficiaries. | Gains compound tax-free within the insurance policy wrapper. |

| Succession & Probate | Subject to complex probate processes depending on the physical jurisdiction of assets. | Pays out immediately as a death benefit, completely bypassing probate delays. |

| Asset Protection | Vulnerable if “sham trust” arguments succeed or the corporate veil is pierced. | Highly robust; assets belong to the insurer, shielding them from the policyholder’s personal creditors. |

| Reporting Privacy | CRS/FATCA reporting often identifies the Ultimate Beneficial Owner (UBO) directly. | Compliant reporting occurs, but privacy is enhanced as the insurer acts as the legal owner. |

Intergenerational Wealth Transfer and Liquidity

When a PPLI policy is integrated with a trust—creating an Irrevocable Life Insurance Trust (ILIT)—it establishes the ultimate succession mechanism. Upon the demise of the insured patriarch or matriarch, the assets liquidate and pay out to the trust as a tax-free death benefit.

This mechanism provides immediate, frictionless liquidity. Liquidity planning remains one of the most overlooked elements of wealth management. For families whose wealth is heavily concentrated in illiquid operational businesses, private equity, or real estate, the sudden imposition of estate taxes or the need to buy out divergent family branches upon the founder’s death can force the catastrophic fire-sale of core assets at depressed valuations. Strategic insurance solutions bridge this gap, injecting cash directly into the estate precisely when it is needed to stabilize the family enterprise.

Furthermore, as the OECD’s BEPS 2.0 framework and Pillar Two global minimum tax rules prompt UHNW clients to reassess their cross-border structures, PPLI wrappers are increasingly recognized as a fully compliant, tax-efficient solution within the new regulatory landscape.

Family Governance, Philanthropy, and Next-Generation Stewardship

Financial structures and legal firewalls are ultimately futile if the family itself fragments. Industry wisdom and historical data continually demonstrate that severe wealth erosion by the third generation is rarely the result of poor macroeconomic conditions or weak investment performance; rather, it is caused by familial conflict, lack of preparation, and ambiguous succession mandates. Consequently, the Singapore wealth management paradigm has expanded to incorporate rigorous family governance consulting.

Constitutions and the Architecture of Trust

Family governance is the non-financial infrastructure that sustains wealth. It is not merely bureaucracy, but the deliberate building of an “architecture of trust”. In Singapore, there is a pronounced trend toward the formalization of Family Constitutions and Governance Charters.

A family constitution serves as the foundational document, delineating the family’s shared values, historical narrative, and long-term vision. It separates the “owner identity” (the unique characteristics and values of those holding the capital) from the “investor identity” (the risk appetite and strategic deployment of that capital). While a constitution outlines the philosophical bedrock, a Governance Charter provides the operational framework, instituting mechanisms like Family Councils.

The Family Council acts as a board of directors for the family itself, establishing clear protocols for conflict resolution, voting rights, dividend distribution policies, and strict employment criteria for next-generation members wishing to enter the family business. By designing these structures during periods of stability, families replace emotional reactivity with procedural certainty, preventing individual disputes from escalating into destructive litigation.

The Philanthropic Imperative and the PTIS

Philanthropy has evolved from ad-hoc charitable giving to a structured, impact-driven mechanism for family cohesion and next-generation training. It provides a neutral, lower-risk environment for younger family members to learn capital allocation, board governance, and project evaluation without jeopardizing the core operating business.

To incentivize structured giving and solidify its position as “Asia’s Centre for Philanthropy,” Singapore introduced the Philanthropy Tax Incentive Scheme (PTIS), which took effect in January 2024 and remains a critical tool in 2026. Under the PTIS, qualifying donors managing funds via a Section 13O or 13U SFO can claim a 100% tax deduction for overseas donations made through approved local intermediaries, capped at 40% of the donor’s statutory income, for a period of five years. This landmark policy aligns the family’s global philanthropic ambitions with profound domestic tax efficiency, allowing capital to flow to international causes without incurring a local tax penalty. Concurrently, the 250% tax deduction for qualifying domestic donations to Institutions of a Public Character (IPCs) has been extended through December 31, 2029, reinforcing domestic charitable initiatives.

Technological Integration: AI and ESG

The incoming generation of wealth stewards is distinctly focused on digital innovation and Environmental, Social, and Governance (ESG) mandates. Family offices are heavily transitioning portfolios toward climate-related investments and blended finance structures, optimizing the MAS capital deployment requirements under the 13O/13U schemes.

Simultaneously, Artificial Intelligence (AI) is being deployed at scale within SFOs to optimize portfolio rebalancing, execute real-time risk analytics, and manage complex cross-border compliance reporting. Reflecting its proactive regulatory stance, Singapore launched the world’s first Model AI Governance Framework for Agentic AI in January 2026 at the World Economic Forum.

This framework requires family offices and financial institutions to assess risks upfront, evaluate data sensitivity, and implement robust technical controls such as sandboxing and privilege escalation protections. Crucially, the framework mandates “meaningful human accountability,” ensuring that while AI agents can execute complex portfolio adjustments or compliance checks, human oversight remains central to all approval checkpoints. Adhering to these technological guardrails ensures that family offices remain agile and data-driven without exposing themselves to systemic cyber or regulatory risks.

Conclusion

The private wealth management ecosystem in Singapore has decisively transitioned from an offshore booking center to a sophisticated, highly regulated hub for global capital structuring and generational stewardship. The frameworks analyzed—the enhanced Section 13O and 13U tax incentives with their strict economic substance requirements, the structural agility of the Variable Capital Company, the robust asset protection of the Trustees Act firewalls, the tax efficiency of Private Placement Life Insurance, and the institutionalization of family governance—do not operate in isolation.

They are interlocking gears within a comprehensive wealth preservation strategy.

For high-net-worth families, the implications are unambiguous. The era of regulatory leniency, opaque holding structures, and passive capital has permanently concluded. It has been replaced by an environment that demands economic substance, rigorous AML compliance, and transparent governance.

However, in exchange for meeting these high thresholds, families gain access to an unparalleled architecture of legal certainty, fiscal stability, and strategic flexibility. By deliberately integrating these legal, financial, and governance instruments, UHNW families can secure their operational continuity, protect their assets against volatile geopolitical and legal risks, and ensure the successful, unified stewardship of their legacy across generations.

Related reading

- Explore all blog articles

- About Arjan KC

- Singapore Wealth Management for UHNW Families

-

[Tampa Nursing Home Abuse & Neglect Lawyers Legal Guide](/blog/tampa-nursing-home-neglect-attorney-guide/)