Fintech India Digital Marketing Report: Startups & Trends

Digital Marketing for Fintech Startups in India

Industry Overview

Brief Description of Fintech Startups in India

The Indian financial technology (fintech) ecosystem has undergone a profound structural metamorphosis, evolving from a nascent sector focused primarily on basic digital payments into a highly sophisticated, multi-vertical digital economy. As of 2025, India hosts the third-largest fintech ecosystem globally, characterized by the presence of over 9,000 active fintech firms operating across a highly diversified landscape. These entities span an extensive array of sub-sectors, including digital payments, peer-to-peer (P2P) lending, wealthtech, insurtech, neobanking, regulatory technology (regtech), and embedded finance.

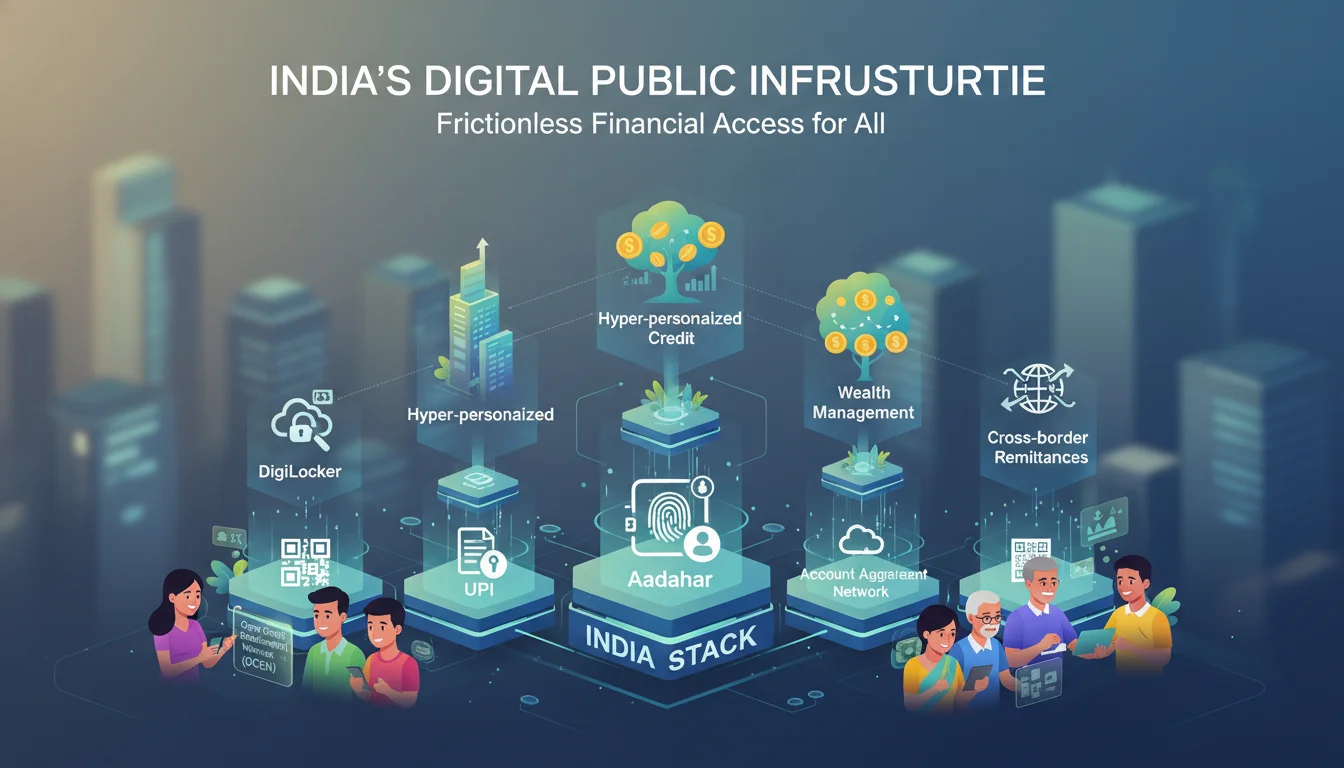

The ecosystem is uniquely underpinned by India’s robust Digital Public Infrastructure (DPI), commonly referred to as the “India Stack.” This architectural framework encompasses foundational elements such as the Unified Payments Interface (UPI), Aadhaar-based biometric identification, electronic Know Your Customer (e-KYC) protocols, DigiLocker, and the highly transformative Account Aggregator (AA) framework. The deployment of the JAM Trinity (Jan Dhan-Aadhaar-Mobile) has enabled startups to bypass legacy financial infrastructure, dramatically reducing customer onboarding friction and facilitating the democratization of financial services across socio-economic strata. Consequently, the modern Indian fintech startup is no longer merely a digital interface for traditional banking; it is a standalone entity capable of hyper-personalized credit underwriting, algorithmic wealth management, and real-time cross-border remittances.

Current Market Size, Growth, and Trends

The financial valuation of the Indian fintech market reflects exponential and sustained growth, driven by progressive regulatory frameworks, massive smartphone penetration, and shifts in consumer behavior. As of 2025, the market is valued at approximately USD 142.5 billion to USD 150 billion. Forecasts indicate a continued aggressive upward trajectory, with conservative projections estimating the market will reach approximately USD 642.9 billion by 2034, representing a Compound Annual Growth Rate (CAGR) of 16.70% over the 2026 to 2034 period. Alternative predictive models suggest an even more aggressive expansion, forecasting a market value of USD 867.6 billion by 2033 at a CAGR of 28.7%, or USD 186.29 billion by 2035 growing at 15.52%.

Several dominant structural trends are currently reshaping the market dynamics and dictating the flow of venture capital:

- Dominance of Digital Payments: Driven by UPI, mobile banking, and peer-to-peer transfers, this segment operates as the primary top-of-funnel acquisition channel for fintechs. Captures over 39% to 42.87% of the total market share, with UPI transactions crossing USD 2 trillion in 2024.

- Artificial Intelligence (AI) & Machine Learning: Deployment of AI for real-time fraud detection, automated credit scoring utilizing alternative data, personalized wealth advisory, and conversational interfaces. Holds an estimated 36% technology market share, valued at USD 53.3 billion, driving underwriting efficiencies.

- Rise of Embedded Finance & Open Banking: Seamless integration of financial products (credit, insurance) at the point of sale within non-financial platforms, facilitated by APIs and the Account Aggregator framework. The embedded finance market is projected to grow from USD 5.75 billion in 2024 to USD 28.6 billion by 2029.

- Ascension of WealthTech and Neobanking: Transitioning users from basic savers to active investors via goal-based investing, fractional ownership, and high-yield digital banking alternatives. Neobanking is projected to grow at a 19.64% CAGR through 2031, with retail end-users dominating consumption.

- Venture Capital Shift to Resilience: Investors have pivoted from funding “growth at all costs” to demanding sustainable unit economics, clear paths to profitability, and predictable monetization models. VC funding reached approximately USD 16 billion in 2025, with larger deals focusing on wealthtech and secured lending.

Key Challenges Faced by Businesses in This Industry

Despite the immense total addressable market, Indian fintech startups operate in a highly constrained environment characterized by structural, regulatory, and behavioral hurdles. The transition from growth to infrastructure has made regulatory compliance a competitive moat, but it simultaneously erects significant barriers to scale.

The regulatory environment is notoriously complex and highly fragmented. Operating a fintech in India requires navigating a web of regulations enforced by multiple bodies, including the Reserve Bank of India (RBI), the Securities and Exchange Board of India (SEBI), the Insurance Regulatory and Development Authority of India (IRDAI), and the Ministry of Electronics and Information Technology (MeitY). Recent years have witnessed the RBI tightening oversight on digital lending directions, banking-as-a-service (BaaS) partnerships, and payment aggregators. Startups managing complex BaaS relationships struggle with unclear divisions of compliance responsibilities, where gaps in accountability can jeopardize entire operational partnerships. Furthermore, the implementation of the Digital Personal Data Protection (DPDP) Act 2023 mandates strict data localization, consent architectures, and privacy frameworks, fundamentally altering how startups collect, store, and process user data.

Customer acquisition costs (CAC) have escalated dramatically. The hyper-competitive nature of the sector, combined with global macroeconomic pressures, has driven performance marketing costs to unsustainable levels. CAC in the fintech sector globally averages around USD 784, and while localized costs in India remain lower (e.g., $15-25 for neobanks), they are rising rapidly. The reliance on performance marketing platforms has resulted in ad cost inflation, shrinking the margin for error for early-stage startups and forcing a shift in focus toward Customer Lifetime Value (LTV) and retention.

Trust deficits and fraud concerns continually undermine consumer confidence. Financial services inherently require extraordinary levels of consumer trust. However, the rise of sophisticated fraud vectors—including synthetic identities, deepfakes, and UPI phishing scams—has severely eroded this trust. Startups face the dual challenge of implementing frictionless, sub-second underwriting and onboarding while simultaneously demonstrating robust Anti-Money Laundering (AML) and Know Your Customer (KYC) controls. Standard identity verification methods often fail for underbanked populations, requiring multi-modal verification architectures.

Finally, the ecosystem grapples with low financial literacy and entrenched cash dependency. While digital infrastructure has scaled exponentially, cognitive adoption lags significantly. Less than 30% of rural users fully comprehend the mechanics of mobile financial instruments, and despite the UPI boom, cash continues to account for over half of all retail transactions. This structural deficiency forces marketing efforts to shoulder the heavy burden of basic financial education before any meaningful product differentiation or conversion can occur.

Digital Landscape in India (Contextual to the Industry)

Internet & Social Media Usage Relevant to Fintech Startups

The bedrock of fintech expansion in India is the unprecedented penetration of digital connectivity. By early 2025, India reported a staggering 1.12 billion cellular mobile connections, equating to 76.6% of the total population. The internet user base stood at 806 million individuals, achieving a nationwide online penetration rate of 55.3%. Within this highly connected demographic, there are 491 million active social media user identities, representing 33.7% of the total population. Crucially for financial service marketers, data published in the ad planning tools of top social media platforms indicates there were 444 million social media users aged 18 and above, forming the primary addressable market for adult financial products, credit facilities, and investment vehicles.

A profound geographical and demographic shift is actively redesigning the digital consumption map. Tier-2 and Tier-3 cities have evolved from peripheral emerging markets into the central epicenters of digital growth. These non-metro regions now account for the largest share of new internet users and contribute nearly 40% to the country’s GDP. With internet penetration in states like Uttar Pradesh and Bihar rising above 45% due to the BharatNet fiber-optic network and the rapid spread of 4G/5G, the urban-rural digital divide is narrowing rapidly. Demand from these regions is no longer experimental; it is active and discerning. Product affordability, local relevance, and practical use cases significantly outweigh metropolitan brand awareness, presenting a massive, untapped reservoir for digital credit, micro-insurance, and regional wealth creation tools.

Popular Platforms Among the Target Audience

The Indian digital consumer’s attention is heavily fragmented across an array of platforms, but video-first and conversational interfaces completely dominate user engagement metrics.

The Meta ecosystem, comprising Instagram and WhatsApp, serves as the primary conduit for discovery and transactional communication. Instagram Reels have become the de facto discovery engine for younger demographics, with short-form video consumption in Tier-2 and Tier-3 cities drastically outpacing metro adoption. WhatsApp, conversely, has transcended basic social communication to become a primary commercial and conversational marketing channel.

With users preferring to utilize WhatsApp for direct conversations over traditional apps, it offers massive potential for automated customer relationship management (CRM), lead nurturing, and financial literacy distribution.

Telegram has emerged as an underutilized but exceptionally potent marketing channel, particularly for specific fintech sub-niches such as cryptocurrency, algorithmic trading, and startup ecosystems. Boasting over 1 billion monthly users globally and adding 2.5 million users daily, Telegram excels at fostering tight-knit, highly engaged communities. In India, it serves as a high-conversion platform for financially savvy early adopters, with channels dedicated to solo founders, SEO strategies, and startup ventures providing direct access to B2B and prosumer audiences.

YouTube remains the cornerstone of financial education in the subcontinent. As the second-largest search engine globally, long-form content explaining mutual funds, taxation structures, and stock market fundamentals commands immense, sustained viewership. YouTube serves as the primary top-of-funnel acquisition channel for wealthtech platforms, where educators and analysts build the requisite trust before transitioning viewers into active platform users.

Consumer Online Behavior Related to Fintech Startups

Generational Financial Behavior Matrix

| Behavioral Dimension | Millennials | Generation Z |

|---|---|---|

| Core Financial Motivations | Focus on long-term wealth accumulation, debt reduction, and familial financial security. Highly shaped by past economic downturns. | Value-driven spending, digital convenience, and experiencing life over asset ownership. Highly focused on ethics and brand transparency. |

| Preferred Financial Instruments | Systematic Investment Plans (SIPs), real estate, retirement funds, traditional digital gold, and secure, low-risk avenues. | Buy Now, Pay Later (BNPL) services, high-risk/high-reward equities, cryptocurrencies, fractional ownership, and digital wallets. |

| Digital Marketing Receptivity | Receptive to comprehensive dashboards, email newsletters, long-form educational blogs, and traditional SEO-driven research. | Highly receptive to influencer marketing, peer recommendations, short-form video (Reels/TikTok), and seamless, cashless transactions. |

| Trust Signals | Institutional backing, clear regulatory compliance, historical performance data, and robust security protocols. | Authenticity, social proof from trusted creators, social media engagement, and immediate, frictionless user experiences. |

Furthermore, a critical behavioral trend dominating the market is the “vernacular shift.” Users in non-metro areas heavily prefer consuming content and making purchase decisions in their native languages. Voice search adoption rates in Tier-2 and Tier-3 cities are significantly higher than in metros, indicating that typing in English poses a friction point. Consequently, fintech interfaces and marketing campaigns must integrate voice-first, localized search engine optimization (SEO) across languages like Hindi, Tamil, and Bengali to capture this massive surge in regional intent.

Digital Marketing Opportunities

How Digital Marketing Can Solve the Key Challenges

In the fintech sector, the product is intrinsically intangible; users are essentially purchasing promises of security, growth, or liquidity. Digital marketing acts as the critical bridge translating these complex, heavily regulated financial products into accessible, trustworthy consumer experiences.

Digital marketing directly combats the challenge of escalating Customer Acquisition Costs (CAC) through the cultivation of organic trust. By investing heavily in technical Search Engine Optimization (SEO) and high-quality, authoritative educational content, startups can attract high-intent users organically. This strategy effectively bypasses the auction-based inflation inherent in Meta and Google advertising networks, fundamentally shifting the unit economics from short-term ad dependency to long-term compounding organic equity.

Furthermore, strategic digital marketing addresses the industry’s pervasive trust deficit. Marketing frameworks that prioritize radical transparency—such as clear fee disclosures, founder-led communication narratives, and explicit showcases of data security compliance (e.g., ISO certifications, GDPR/DPDP alignment, TRUSTe marks)—transform regulatory burdens into competitive marketing moats. When consumers view a brand as a compliant, secure educator rather than a predatory vendor, friction during the KYC and onboarding phases drastically reduces.

Finally, digital marketing solves the crisis of financial illiteracy. In a country where only 27% of the population is deemed financially literate, traditional feature-based advertising falls flat. Content marketing shoulders the burden of education by breaking down complex financial jargon into digestible, vernacular formats. By educating the user first through bite-sized videos and interactive tools, the startup positions itself as a trusted fiduciary advisor.

Best Strategies for Fintech Startups in India

Content Marketing, Education, and Generative Engine Optimization (GEO)

In the “Your Money or Your Life” (YMYL) sector, content is subjected to extreme scrutiny by search engine algorithms. Content cannot merely be engaging; it must be authoritative, highly accurate, and written by demonstrated experts adhering to E-E-A-T (Experience, Expertise, Authoritativeness, and Trustworthiness) principles. The most successful fintech marketing strategies in India operate on an “education-first” paradigm. Producing comprehensive investment guides, tax calculation tools, and macroeconomic analysis builds insurmountable domain authority. Furthermore, the integration of Generative Engine Optimization (GEO) is becoming paramount. As users increasingly rely on Large Language Models (LLMs) like ChatGPT for financial queries, startups must structure their proprietary data, verifiable evidence, and API documentations so that AI systems recognize and cite them as factual, primary sources.

Search Engine Optimization (SEO) and Vernacular Localization

SEO in fintech must be aggressively targeted and technically flawless. The strategy is bifurcated into capturing high-intent transactional queries (e.g., “apply for MSME business loan online”) and broad informational queries designed to capture users early in the funnel. Establishing a robust technical SEO architecture—ensuring sub-second mobile load times, strict HTTPS security, and deploying structured schema markup for financial products—is mandatory. More importantly, the integration of vernacular SEO unlocks the Bharat demographic. By focusing on localized, long-tail queries in Hindi, Tamil, or Bengali, and optimizing for regional voice search tendencies, startups can tap into the rapidly expanding Tier-2 and Tier-3 markets where competition from English-centric legacy banks is weak.

Micro-Influencer and Community-Led Marketing

The era of relying solely on exorbitant celebrity endorsements to build trust is waning, replaced by a demand for authentic expertise. Fintechs are achieving superior Return on Investment (ROI) by deploying “finfluencers”—micro-influencers and regional content creators who possess deep, niche credibility and highly engaged audiences. Compensation models have shifted, with 53% of brands utilizing performance-based structures, mitigating risk while aligning creator incentives with actual user acquisition. For B2B fintech platforms, leveraging founders, CFOs, and finance leaders as micro-influencers on LinkedIn to share operational insights has proven highly effective for lead generation without the need for paid ads. Concurrently, building proprietary communities on platforms like Telegram or WhatsApp fosters immense brand loyalty, provides real-time feedback loops, and encourages organic, word-of-mouth acquisition.

Performance Marketing with Strict Unit Economic Discipline

Paid advertising remains a necessary component for rapid scaling but requires rigorous mathematical discipline. Startups must meticulously define their unit economics—specifically the ratio of Customer Lifetime Value (LTV) to Customer Acquisition Cost (CAC), and the payback period—before scaling ad spend. Utilizing AI-driven programmatic advertising allows for continuous dynamic creative testing, matching specific financial products to hyper-segmented audiences based on real-time behavioral data. Furthermore, utilizing pre-approved compliance templates ensures that marketing teams can iterate rapidly without running afoul of regulatory guardrails.

Local and Global Examples/Case Studies

CRED: Luxury Positioning and Cultural Virality

CRED revolutionized the saturated, mass-market digital payments space by adopting a counter-intuitive strategy: deliberate exclusivity.

CRED

Founded to reward timely credit card payments, CRED restricted its user base strictly to individuals with a credit score of 750 and above. By positioning simple bill payment as a luxury, aspirational experience, CRED cultivated a “trust-tech” platform for India’s most affluent consumers. Their marketing engine relies on highly creative, nostalgic, and viral campaigns (such as the famous “Indiranagar Ka Gunda” advertisement) that generate millions of organic impressions and cultural memes. Despite traditionally high acquisition costs in the premium segment, this strategy has resulted in a highly engaged user base of over 13 million, capturing roughly 20% of India’s total credit card payment volume, while simultaneously reducing their CAC by 40% through organic reach and referral gamification.

Zerodha: Content-Led Organic Supremacy

Zerodha, India’s largest discount brokerage, achieved market leadership without relying on the massive advertising budgets typical of financial institutions. Their marketing strategy is fundamentally rooted in education through their proprietary platform, Varsity. By providing free, high-quality, and structurally organized courses on investing and personal finance, Zerodha organically captured immense high-intent search traffic. This education-first approach built profound trust with retail investors, establishing absolute market leadership with near-zero customer acquisition costs, proving that high-quality content functions as an impenetrable economic moat.

PhonePe: Omnichannel Mass Penetration and Ecosystem Cross-Selling

PhonePe deployed aggressive, ubiquitous marketing campaigns to establish dominance in the digital payments landscape. By leveraging massive media properties, including national television and sponsorships of high-visibility sports tournaments like the IPL, campaigns such as ‘PhonePe Karo’ highlighted the extreme convenience of cashless transactions. However, their true strategic brilliance lies in cross-selling. Once users are acquired via high-frequency, low-margin UPI transactions, PhonePe’s marketing machinery transitions them into an integrated super-app ecosystem, effortlessly cross-selling higher-margin financial services such as insurance, wealth management, and lending.

Groww: Millennial UI/UX and Influencer Synergy

Entering a market dominated by legacy brokers and early disruptors, Groww carved out a leading position by targeting first-time, younger investors. They achieved this through a relentless focus on a clean, intuitive, mobile-first UI/UX that eliminated the intimidation factor of traditional trading. To drive acquisition, Groww aggressively partnered with YouTube financial educators and micro-influencers (such as Pranjal Kamra and CA Rachana) to demystify mutual funds and equity investments. This synergy of an accessible product and relatable, educational marketing resulted in a robust investor base exceeding 50 million users, predominantly under the age of 40.

4. Competitive Analysis

Current Digital Presence of Top Fintech Businesses in India

The Indian fintech landscape is characterized by intense concentration at the top, where a handful of scaled, “winner-take-most” players command the vast majority of consumer attention and digital real estate.

The Payments Duopoly

PhonePe and Google Pay currently monopolize the UPI transaction volume landscape. Their digital presence is ubiquitous, utilizing a mix of pervasive offline QR code placement, aggressive app store optimization, and continuous push-notification marketing to maintain daily active engagement. Paytm, despite navigating significant regulatory actions regarding its payments bank in early 2024, maintains a formidable presence. It has executed a strategic pivot towards an open-architecture, multi-bank payments platform. Paytm’s physical and digital presence is deeply entrenched via its deployment of over 1.4 crore Soundbox devices and Point-of-Sale (PoS) systems, which serve as high-margin “hooks” to lock in over 40 million merchants, subsequently facilitating lucrative merchant lending opportunities.

WealthTech Leaders

Zerodha and Groww dominate the digital wealth management and discount brokerage space. Their digital footprint is heavily skewed toward SEO dominance and educational content marketing. While Zerodha relies on the massive organic authority of its Varsity platform, Groww utilizes aggressive influencer marketing and App Store Optimization (ASO) to maintain its position at the top of financial app download charts.

Lending and Credit Disruptors

Platforms such as LendingKart, KreditBee, and ZestMoney maintain an aggressive digital posture across performance marketing channels (Meta, Google Ads). They target the MSME and unbanked consumer segments by heavily promoting alternative credit scoring and instant disbursal capabilities, utilizing programmatic ads to capture high-intent users actively searching for liquidity.

What They Are Doing Well

Incumbents across all verticals excel in engineering frictionless, dopamine-driven onboarding experiences. They have successfully integrated behavioral economics into their product marketing, heavily utilizing gamification—through dynamic cashbacks, randomized scratch cards, and tiered loyalty rewards—to drive daily active usage and habitual platform interaction.

Technologically, these platforms possess highly sophisticated data pipelines and machine learning algorithms that allow them to cross-sell financial products with extreme efficiency. Their marketing communication is highly automated, deploying contextual push notifications based on real-time transaction data. Furthermore, their sheer scale provides them with massive brand recall, reinforced by hundreds of millions of dollars deployed across high-visibility properties, ensuring they remain top-of-mind for the average Indian consumer.

Gaps and Opportunities to Outperform Them

Despite their vast resources and market share, the rapid scaling of these top-tier fintechs has created critical structural vulnerabilities and service gaps, presenting immediate arbitrage opportunities for agile, user-centric startups:

| Competitive Gap | Incumbent Failing | Startup Opportunity |

|---|---|---|

| The “Human-First” Support Deficit | Over-reliance on cost-saving automated chatbots and convoluted IVR systems leads to massive user frustration during transaction disputes. | Market a “Human-First Customer Support” model. Providing clear transaction histories, visible money flow records, and access to human agents in regional languages builds immense trust and yields significantly higher retention rates. |

| Cognitive Overload in Super-Apps | Platforms like Paytm have evolved into bloated super-apps, creating cluttered interfaces that confuse users attempting basic tasks, diluting core brand messaging. | Focus on unbundling the super-app. Build hyper-focused, minimalist applications that solve one specific problem exceptionally well (e.g., dedicated Gen Z micro-investing or B2B invoice discounting), winning on superior UI/UX and clarity. |

| The Superficial Vernacular Approach | Incumbents often treat regional markets with superficial translation overlays, failing to grasp local cultural nuances or digital behaviors. | Build natively vernacular products. Integrate voice-assisted onboarding and culturally resonant design tailored specifically to the unique consumption habits of Tier-2 and Tier-3 consumers, moving beyond translation to genuine empathy. |

| Data Monopolies vs. Open Finance | Incumbents built their moats by hoarding proprietary transaction data, making user porting difficult. | Leverage the Account Aggregator (AA) framework. Startups can now access a user’s comprehensive, verified financial history (with consent). This allows them to market highly personalized, risk-adjusted loan rates or bespoke portfolio strategies, breaking the data monopoly of legacy giants. |

5. Recommended Strategy for Fintech Startups in India

To navigate the hyper-competitive, high-CAC, and heavily regulated environment of 2026, new fintech entrants must abandon the indiscriminate “spray and pray” advertising models. Instead, they must deploy a highly targeted, trust-centric digital marketing framework that leverages community, compliance, and hyper-personalization.

Target Audience Personas

To maximize marketing efficiency, campaigns must be ruthlessly segmented. The following personas represent high-growth, underserved cohorts:

Persona A: The Aspiring “Bharat” Entrepreneur (Tier-2/3 MSME Owner)

- Age/Location: 28–45 years old; based in emerging economic hubs like Jaipur, Indore, Surat, or Coimbatore.

- Psychographics & Preferences: Highly price-conscious and deeply values community reputation and word-of-mouth validation. Relies almost exclusively on WhatsApp for daily business operations. Prefers consuming content and conducting transactions in regional languages (Hindi, Gujarati, Tamil).

- Pain Points: Lacks a formal credit history suitable for legacy banks, struggles with working capital flow, and is highly skeptical of hidden processing fees or aggressive collection tactics.

- Marketing Approach: Vernacular video testimonials featuring similar local business owners. Deployment of localized Facebook ads. Voice-search optimized content detailing how alternative data (like GST returns) can secure loans via the Account Aggregator framework.

Persona B: The Digitally Native Wealth Builder (Gen Z / Young Millennial)

- Age/Location: 18–30 years old; based in Tier-1 metros and emerging tech hubs (Bengaluru, Pune, Hyderabad).

- Psychographics & Preferences: Mobile-first, inherently distrustful of traditional banking bureaucracy. Highly active on Instagram and Telegram. Decision-making is heavily influenced by peer reviews and trusted finfluencers.

Expects instantaneous, frictionless UI/UX and values ethical, transparent brand identities.

- Pain Points: Overwhelmed by traditional financial jargon. Suffers from investment “FOMO” regarding emerging asset classes but fears market volatility.

- Marketing Approach: Bite-sized, highly visual educational Reels. Interactive financial calculators. Gamified referral programs. Community-led growth and exclusive updates distributed via proprietary Telegram channels.

Recommended Channels and Campaign Types

Conversational CRM via WhatsApp

Marketing must transition from broadcast to dialogue. Utilizing the WhatsApp Business API allows startups to deliver personalized financial health reports, interactive payment reminders, and seamless onboarding assistance directly within the user’s preferred app. Transitioning the tone from corporate mandates (“Your payment is due”) to collaborative partnerships (“Want us to auto-pay this for you?”) radically improves Customer Experience and reduces app uninstalls.

Hyper-Local Programmatic Digital Out-of-Home (DOOH)

The Indian DOOH market is expanding rapidly into Tier-2 cities. Startups can utilize programmatic platforms to buy hyper-local ad slots dynamically. Syncing offline digital billboard exposure in smart cities with mobile retargeting ensures the brand appears ubiquitous to a geographically fenced audience, significantly boosting the conversion rates of subsequent digital ads.

Micro-Influencer Pods and Vernacular Storytelling

Rather than exhausting the budget on a single macro-celebrity, capital should be deployed across 50–100 regional micro-influencers (10k–50k followers). These creators generate authentic, relatable tutorials (e.g., demonstrating a micro-saving app in Kannada or explaining invoice discounting in Tamil). This strategy builds a massive “trust loop” and drives significantly higher engagement and conversion rates at a fraction of the cost.

Content Ideas Specific to Fintech in India

- “De-Jargonizing” Video Series: Produce high-velocity, short-form vertical videos (YouTube Shorts, Instagram Reels) that explain complex terms (e.g., “What is a Repo Rate?”, “How does compound interest affect your SIP?”, or “Understanding Account Aggregators”) in under 60 seconds, presented natively in Hindi, Tamil, and English.

- Interactive Financial Health Calculators: Develop free-to-use, highly intuitive web tools such as Retirement Planners, EMI Calculators, SIP Return Estimators, and GST Tax Calculators. These function as massive lead-generation magnets and attract highly qualified organic backlinks from financial bloggers.

- Founder-Led Transparency Reports: Publish monthly blog posts or comprehensive LinkedIn threads detailing the startup’s operational metrics, regulatory compliance efforts, and product roadmap. In an industry plagued by a severe trust deficit, radical transparency serves as a highly potent marketing differentiator, appealing directly to B2B clients and discerning retail investors.

Budget-Friendly Digital Marketing Approaches

For early-stage fintechs where capital efficiency and burn rate are heavily scrutinized, marketing must be lean and measurable.

- Community Incubation on Telegram and Reddit: Building active, moderated communities on platforms like Telegram or specific subreddits costs nothing but time and domain expertise. Hosting weekly “Ask Me Anything” (AMA) sessions on personal finance or startup building cultivates a fiercely loyal cohort of early adopters who serve as free, organic brand evangelists.

- Performance-Based Affiliate Networks: Partner with independent financial bloggers, CAs, and student ambassadors, offering them a Cost-Per-Acquisition (CPA) or lead-generation bounty for every successful KYC-approved user they drive. This ensures marketing dollars are deployed exclusively on actual revenue-generating activities, preserving cash flow.

- Pre-Launch SEO Compounding: Recognizing that SEO takes time to compound, startups should launch a heavily optimized financial blog 3-6 months before the actual application goes live. This ensures that upon release, the startup already possesses a steady stream of organic, zero-CAC traffic ready to be monetized.

Keywords & SEO Opportunities

Fintech SEO in India is inherently complex. Because the sector falls under Google’s strict YMYL (Your Money or Your Life) guidelines, content is evaluated against rigorous E-E-A-T standards. Thin content or anonymous authorship will result in algorithmic suppression. The strategy must carefully balance high-volume discovery queries with highly specific, commercial-intent long-tail keywords, while also preparing for the shift toward AI-driven Generative Engine queries.

High-Intent Keywords for Ranking (Transactional & Bottom-of-Funnel)

These keywords represent users at the bottom of the funnel (BoFu) who have identified their specific financial problem and are actively seeking a vendor to execute a transaction. While competition is fierce, they yield the highest conversion rates and lowest payback periods.

| Fintech Vertical | Primary High-Intent Keywords | Associated Search Intent & Context |

|---|---|---|

| Lending & Credit | “instant personal loan app”, “business loans for MSME online”, “lowest interest personal loan 2026”, “startup business loans” | Immediate financial liquidity required; high readiness to submit documents or link accounts via the AA framework. |

| Wealth & Investment | “open demat account zero brokerage”, “best SIP for 5 years”, “buy direct mutual funds online”, “best mutual funds to invest in 2026” | Wealth creation initiation; users are actively comparing platform fees, historical returns, and UX design. |

| Payments & B2B SaaS | “best B2B payment gateway India”, “UPI API for small business”, “cross border remittance app”, “automated payout API” | Integration of financial infrastructure; seeking high reliability, robust API documentation, and low transaction fees. |

| InsurTech | “affordable health insurance for family”, “term life insurance premium calculator”, “buy car insurance online instant” | Risk mitigation; users are highly sensitive to premium costs and claim settlement ratios. |

Long-Tail Keyword Opportunities (India-Specific & Vernacular)

Long-tail keywords (phrases containing four or more words) account for approximately 70% of all search queries in India. They face significantly lower competition, exhibit higher conversion intent, and are critical for startups attempting to capture highly specific niches, particularly when targeting regional markets or leveraging the conversational nature of Generative AI search prompts.

-

Geo-Specific & Vernacular Modifiers: Indian users frequently use dual-language searches or specific local modifiers.

- “affordable health insurance for family in [City Name]”

- “how to apply for working capital loan in Tamil”

- “best zero balance savings account for students in Maharashtra”

- “business loan low interest rate in”

-

Problem-Solution Specific (Generative Engine Prompts): As users shift to ChatGPT or Google SGE, keywords resemble conversational questions outlining specific business parameters.

- “what are the best digital lending platforms for unbanked gig workers in India?”

- “how to automate GST filing and vendor payouts for Indian e-commerce”

- “compare mutual fund returns 2025 vs 2026 for conservative investors”

- “which corporate card solution helps Indian tech startups manage expense reporting?”

Implementation Roadmap

A disciplined, highly structured phased approach is vital. It prevents capital misallocation and ensures that marketing efforts scale precisely in tandem with product stability, regulatory compliance mandates, and fundraising milestones.

Short-Term Quick Wins (1–3 Months): Foundation, Compliance & Validation

The initial quarter is dedicated to establishing the unglamorous but essential operational infrastructure, mitigating all compliance risks, and executing low-cost customer acquisition experiments to validate unit economics.

Month 1: Infrastructure, Compliance, and Technical SEO

-

Regulatory Guardrails: Establish pre-approved creative templates with the legal department.

- Standardized Claims and Disclosures: This includes standardized claims, mandatory disclaimers, and RBI/SEBI disclosures to ensure campaigns can launch in days rather than weeks.

- Corporate Compliance Alignment: Ensure foundational legal requirements necessary for institutional trust are met—such as completing DPIIT recognition for tax benefits, verifying FC-GPR filings for foreign investments, and ensuring TDS returns are current. Non-compliance here creates major funding obstacles and reputational damage.

- Technical SEO: Implement foundational technical SEO architecture, ensuring strict HTTPS security, optimizing for sub-second mobile page loads, deploying structured schema markup for all financial product pages, and launching core YMYL-compliant educational pillar content.

- Unit Economics Baseline: Define strict tracking parameters within the MarTech stack: establish baseline metrics for Customer Acquisition Cost (CAC), Lifetime Value (LTV), payback periods, and KYC drop-off rates.

Month 2: Community Incubation & Owned Media Activation

- Community Launch: Establish an exclusive WhatsApp or Telegram community offering daily market insights, tax tips, or business growth strategies, aiming to seed the initial 1,000 highly engaged early adopters organically.

- Micro-Influencer Pilot: Initiate a controlled micro-influencer pilot program targeting 10–15 niche finfluencers (e.g., regional CAs or personal finance vloggers) on YouTube and Instagram to test messaging resonance and track initial conversion velocity.

- API and AA Integration: Finalize backend integrations with the Account Aggregator framework to ensure that once marketing drives a lead, the subsequent data-sharing and underwriting process is completely frictionless.

Month 3: Performance Marketing Alpha Testing

- Test-and-Learn Spend: Allocate 10–15% of the total marketing budget to execute controlled, programmatic test-and-learn ad cycles across Meta, Google, and localized display networks.

- Data Analysis: Rigorously analyze the initial acquisition data to identify the lowest-CAC channels, refine the Ideal Customer Profile (ICP), and optimize the ad creative based on real-time engagement metrics.

Long-Term Strategy (6–12 Months): Scaling, Retention & Omnichannel Dominance

Once product-market fit is confirmed and unit economics demonstrate a viable path to profitability, the focus shifts aggressively to scaling acquisition, deepening retention strategies, and expanding market boundaries.

Months 4–6: Scaling Content, Vernacular Reach, and Affiliates

- Vernacular Expansion: Dramatically ramp up the production of localized, vernacular content targeting Tier-2 and Tier-3 search queries, ensuring all app interfaces and support documentation are natively translated.

- Tool Deployment: Deploy interactive financial tools (calculators, tax estimators) across the website to capture mid-funnel organic traffic and build a robust, authoritative backlink profile.

- Affiliate Transition: Transition successful micro-influencer campaigns into long-term, performance-based affiliate partnerships to lock in predictable acquisition costs.

Months 7–9: Embedded Finance and Deep Personalization

- B2B2C Integration: Execute strategic co-marketing campaigns with non-financial platforms to integrate embedded finance solutions (e.g., offering point-of-sale credit on regional e-commerce sites or instant financing within mobility apps).

- AA-Driven CRM: Leverage the Account Aggregator data to launch highly personalized email and WhatsApp retention campaigns. Move beyond generic newsletters to offer customized financial products (e.g., portfolio rebalancing or targeted loan top-ups) based on a user’s verified, real-time financial behavior.

Months 10–12: Advanced Automation and Investor Readiness

- Marketing Operations Automation: Fully integrate AI-driven marketing automation across the funnel to personalize the entire customer journey, specifically targeting the reduction of app uninstalls and increasing the velocity of cross-selling.

- Omnichannel Presence: Expand digital advertising targeting into hyper-local programmatic DOOH networks in emerging smart cities to reinforce physical brand presence.

- Data Room Preparation: Conduct a comprehensive audit of the blended LTV/CAC ratio, retention cohorts, and overall marketing ROI. Present this optimized, data-driven narrative to prepare the management information system (MIS) for subsequent Series A or B fundraising rounds.

Conclusion

The Indian fintech sector has officially transitioned from an era defined by unchecked, venture-fueled user acquisition into a highly mature phase that demands operational resilience, absolute regulatory compliance, and sustainable unit economics. The landscape is vast, projected to scale into the hundreds of billions, yet it remains fraught with sophisticated fraud, stringent data privacy laws, and the exorbitant costs associated with battling incumbent super-apps for consumer attention. In this complex environment, digital marketing is no longer merely a superficial mechanism for top-of-funnel brand awareness; it is the core strategic engine for establishing domain authority, navigating compliance mandates, and driving long-term enterprise value.

For startups operating in India, the integration of deep educational content, hyper-localized vernacular SEO, disciplined performance marketing, and community-driven advocacy is not optional—it is an existential requirement. Startups must leverage open finance architectures like the Account Aggregator framework to deliver hyper-personalized experiences, utilize Telegram and WhatsApp to build trust-centric communities, and deploy micro-influencers to bridge the financial literacy gap in Tier-2 and Tier-3 cities.

Executing this complex, multi-layered strategy requires highly specialized expertise that seamlessly bridges technical marketing acumen with a profound understanding of South Asian digital consumer behavior and regulatory nuances. For fintech startups seeking to operationalize these strategies and build an impenetrable digital moat, partnering with a specialized agency is a critical growth multiplier. Gurkha Technology, a leading, award-winning digital marketing and technology firm based in Nepal, possesses the precise expertise necessary to navigate this complex landscape. With a robust portfolio in scalable SEO, performance-driven digital marketing, complex technical web development, and regional content strategy, Gurkha Technology is uniquely equipped to help financial brands optimize their digital infrastructure. By partnering with Gurkha Technology, startups can drastically reduce their customer acquisition costs, accelerate their growth trajectory across the Indian subcontinent, and ensure their marketing investments translate directly into compliant, scalable, and highly profitable user ecosystems.