Digital Marketing for Indian Insurance: Strategies & Trends

Industry Overview

Brief Description of the Insurance Companies in India

The Indian insurance sector represents one of the most dynamic, heavily regulated, and rapidly evolving financial markets in the global economy. Historically characterized by state-owned monopolies such as the Life Insurance Corporation of India and a reliance on traditional, face-to-face agency models, the landscape has undergone a profound structural transformation. Today, the market operates under the stringent regulatory oversight of the Insurance Regulatory and Development Authority of India (IRDAI), comprising a diverse and highly competitive ecosystem of fifty-seven primary insurers. This cohort is divided into twenty-four entities operating exclusively within the life insurance segment and thirty-three in the general (non-life) insurance space, which encompasses specialized health, agriculture, motor, and property insurers, alongside major reinsurers.

The defining characteristic of the contemporary Indian insurance market is the convergence of traditional financial prudence with aggressive technological disruption. Legacy insurers are increasingly forced to modernize their massive operational infrastructures, while a new breed of digital-native Insurtech companies is fundamentally altering distribution models, underwriting processes, and customer engagement frameworks. This industry operates across a vast and demographically complex geography, requiring insurers to cater simultaneously to high-net-worth urban populations seeking sophisticated wealth-management products and rural demographics requiring highly subsidized, bite-sized risk mitigation tools.

Current Market Size, Growth, and Trends

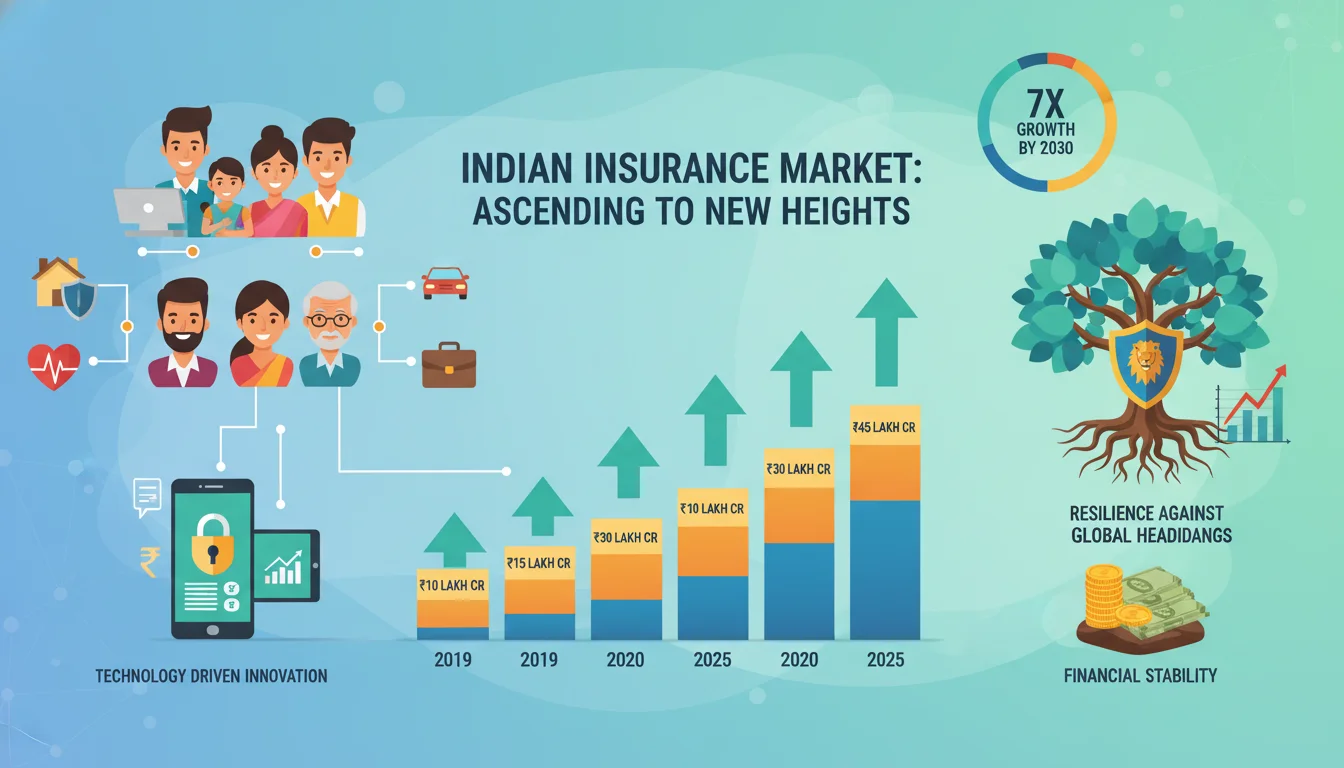

The domestic Indian insurance market has demonstrated exceptional resilience and robust demand, expanding at a Compound Annual Growth Rate (CAGR) of 17% over the past two decades. Driven by rising middle-class incomes, increasing risk awareness catalyzed by the global pandemic, and highly favorable regulatory reforms, the sector’s total market size is projected to reach Rs. 19,30,290 crore (approximately US$ 222.0 billion) by the financial year 2026. According to the Swiss Re Institute, mid-term annual premium growth is forecast at 6.9% between 2026 and 2030, positioning India to outpace the United States, China, and Western Europe to become the strongest growing major insurance market globally.

The life insurance segment remains the dominant engine of premium collections. Recent data indicates that new business premiums for life insurance rose to Rs. 40,206 crore (US$ 4.59 billion) in September 2025 alone, with year-to-date collections demonstrating substantial growth to reach Rs. 2,03,668 crore (US$ 23.28 billion). Conversely, the non-life sector is experiencing an accelerated expansion trajectory, recently growing by 15% against a 16.7% increment recorded in the preceding cycle. Health insurance has emerged as the largest segment within the non-life category and is projected to grow at a vigorous annual rate of 12.8% from 2024 to 2028. This surge is fueled by soaring medical inflation, an aging population, and a heightened awareness of healthcare vulnerabilities. Concurrently, motor insurance is expected to grow at 7.9% annually over the same period, stimulated by a revival in automotive sales and the rapid adoption of electric vehicles.

A vital, transformative growth engine within this landscape is the Insurtech ecosystem. India currently hosts over one hundred and fifty active Insurtech players with a cumulative valuation exceeding US$ 15.8 billion. These digital-first entities generated US$ 0.9 billion in revenue in 2024, representing an extraordinary tenfold increase since 2019. Health Insurtechs are leading this charge, accounting for more than 70% of recent funding and securing four of the five largest investment deals in the sector. Furthermore, the Internet of Things (IoT) insurance market in India is forecast to reach Rs. 1,83,120 crore (US$ 21.4 billion) by 2033, growing at an unprecedented 55% annually as telematics and wearable health tech become mainstream.

Several macroeconomic tailwinds and profound regulatory reforms support this growth trajectory. The Indian government’s strategic decision to increase the Foreign Direct Investment (FDI) limit in the insurance sector from 74% to 100% has enabled complete foreign ownership, triggering massive capital inflows into this long-term, capital-intensive industry. Additionally, mega-schemes initiated by the state have fundamentally expanded the base of insured citizens. The Ayushman Bharat scheme aims to provide health cover of Rs. 5 lakh (US$ 6,075) per family per year for secondary and tertiary care hospitalization, while the Pradhan Mantri Fasal Bima Yojana (PMFBY) has driven massive premium income growth in agricultural crop insurance. As of early 2025, over 74.6 crore individuals were covered under micro-insurance schemes like PM Suraksha Bima and PM Jeevan Jyoti Yojana, illustrating the sheer scale of the domestic market.

| Market Segment / Indicator | Current / Projected Value | Key Growth Metric |

|---|---|---|

| Overall Insurance Market (FY26) | Rs. 19,30,290 crore (US$ 222.0B) | 17% Historical CAGR |

| Mid-Term Premium Growth | N/A | 6.9% Annual Growth |

| Online Insurance Market | US$ 555.10 Million | 14.4% CAGR |

| Insurtech Sector Revenue | US$ 0.9 Billion | 10x Increase since 2019 |

| Total Insurtech Valuation | US$ 15.8 Billion | Over 150 Active Players |

| IoT Insurance Market | Rs. 1,83,120 crore (US$ 21.4B) | 55% Annual Growth |

| Health Insurance Sector Growth | N/A | 12.8% Annual |

| Motor Insurance Sector Growth | N/A | 7.9% Annual |

Key Challenges Faced by Businesses in this Industry

Despite the impressive macroeconomic figures, the Indian insurance industry grapples with deeply entrenched systemic challenges. The most glaring metric is the overall insurance penetration rate—measured as the ratio of premium volume to Gross Domestic Product (GDP). In 2023, the national penetration figure stood at roughly 4.0% to 4.2%, with life insurance contributing approximately 3.2% and general insurance a mere 1.0%. This marginal penetration indicates a vast underserved population and highlights the difficulties insurers face in scaling operations outside tier-one urban centers.

The primary challenge is an enduring trust deficit rooted in the intangibility of the product. Insurance is a promise of future protection rather than a physical commodity, making it inherently difficult for consumers to immediately perceive its value. Many Indian consumers remain highly skeptical of insurers due to historically complex policy jargon, hidden exclusion clauses, and a pervasive fear of claim rejections. Policy documents frequently contain convoluted language that creates friction during the purchase journey and fosters resentment when claims arise. Consequently, insurers must work significantly harder to build credibility and educate the market than businesses in retail or consumer goods.

Furthermore, digital insurance operators face astronomically high Customer Acquisition Costs (CAC). The digital arena is intensely competitive, with massive capital continuously poured into performance marketing. Competing with established legacy brands and highly funded aggregators for top search rankings requires heavy investment, and the Cost-Per-Click (CPC) on search engines and social media for high-intent insurance keywords remains prohibitive for many smaller players. This intense competition forces insurers to constantly optimize their funnels to balance acquisition costs against the lifetime value of the policyholder.

Geographic and demographic disparities also present substantial hurdles. While metropolitan and tier-one cities drive the overwhelming majority of premium collections, the vast rural and semi-urban populations lack fundamental financial literacy regarding risk-mitigation tools. In these regions, life insurance is frequently misconstrued purely as a tax-saving instrument or an investment vehicle rather than a critical safety net. Penetrating these markets requires immense resources to localize content, navigate vernacular languages, and deploy physical or phygital distribution networks.

Finally, the industry operates within a highly restrictive regulatory environment. Insurance advertising in India is strictly governed by IRDAI regulations designed to prevent mis-selling and protect consumer data. These rules limit the extent to which insurers can utilize aggressive marketing claims, personalized targeting strategies, or dynamic pricing models without facing severe compliance penalties. The Digital Personal Data Protection Act (DPDPA) further complicates matters by imposing strict parameters on how insurers collect, store, and utilize consumer data, making data-driven marketing significantly more complex.

Digital Landscape in India (Contextual to the Industry)

Internet & Social Media Usage Relevant to Insurance Companies

India’s digital landscape has undergone a tectonic shift, establishing the infrastructural foundation required for the massive scale of online insurance distribution. With an internet user base exceeding 900 million individuals, India represents one of the largest and most dynamic digital economies globally. The defining characteristic of this landscape is the absolute dominance of mobile internet. Over 600 million users access digital services primarily via smartphones, making mobile devices the crucial first touchpoint for insurance discovery, particularly in tier-two and tier-three cities where physical agency networks are sparse.

This mobile-first environment is deeply intertwined with India’s sophisticated digital public infrastructure, most notably the Unified Payments Interface (UPI) and Aadhaar-based electronic Know Your Customer (eKYC) protocols.

The proliferation of UPI AutoPay has revolutionized the sector by enabling frictionless, recurring premium payments, significantly reducing policy lapse rates. Concurrently, Aadhaar-based eKYC allows insurers to verify identities instantly, reducing the time required for policy issuance from several weeks to mere minutes. Within the online insurance market, mobile applications command the largest share, accounting for 56.1% of the channel distribution in 2025, and are projected to be the fastest-growing medium with a 17.1% CAGR through 2031. For instance, legacy insurer Tata AIA successfully breached 1 million app downloads in 2024, underscoring the massive scalability of mobile-centric distribution.

Popular Platforms Among the Target Audience

The choice of digital platforms in the insurance buyer’s journey is highly dependent on the consumer’s position within the marketing funnel, transitioning from broad awareness to high-intent comparison and final purchase.

Search engines, primarily Google, remain the undisputed gateway for modern healthcare and insurance inquiries. The internet is where the majority of new patients and policyholders begin their research, looking up symptoms, financial solutions, and background checks on providers. Research indicates that an overwhelming 90% of digital marketers prioritize their optimization efforts for Google, recognizing that high-intent searches directly correlate with policy sales.

Social media platforms serve dual purposes of brand building and direct response marketing. Meta platforms (Facebook and Instagram) are utilized extensively for segment-specific targeting, leveraging their vast demographic data to push relevant ads based on life events such as marriage or purchasing a vehicle. Moreover, with India’s massive video consumption rates, YouTube has emerged as a critical platform for educational content. Insurers use YouTube to host explainer videos, simplify complex policy documents, and promote financial literacy, addressing the fundamental trust deficit inherent in the industry. For corporate and B2B segments, particularly concerning group health policies and commercial liability covers, LinkedIn remains the premier platform for targeting business owners and human resources professionals.

Beyond traditional search and social media, specialized third-party aggregator platforms like Policybazaar and Coverfox serve as the ultimate digital hubs for the Indian consumer. These platforms satisfy the highly price-sensitive nature of the Indian market by allowing users to compare premiums, analyze claim settlement ratios, and review policy features side-by-side. Aggregators have essentially commoditized certain standard products, forcing insurers to differentiate on digital user experience and brand trust rather than price alone.

Consumer Online Behavior Related to Insurance Companies

The online behavior of the modern Indian insurance buyer is characterized by rigorous research, a demand for extreme convenience, and a paradoxical relationship with technology. Historically, insurance was exclusively a